By VennerRoad, 19th Apr 2016

By VennerRoad, 19th Apr 2016

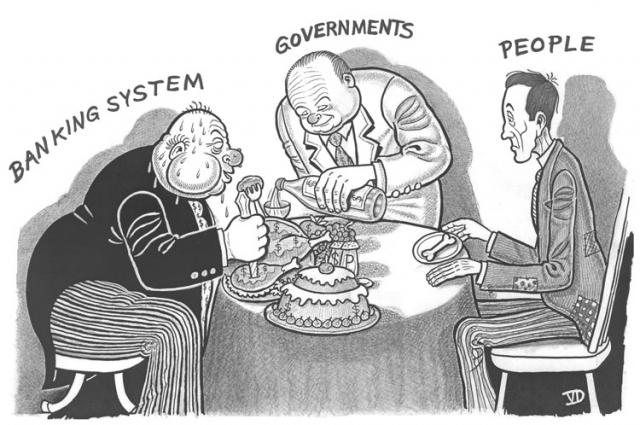

A sadly accurate cartoon.

In recent years, capitalism has had a bad name. Not all criticisms of capitalism are without merit, but the alternative, a command economy, is far, far worse, as the Sutton revelations demonstrate, so we have to either live with what we’ve got, or seek out ways to improve it. Tthe two biggest criticisms usually levelled at capitalism are debt and speculation, so let us take a closer look.

What is a capitalist? Broadly speaking it is an individual who creates wealth, ie creates capital goods, consumer goods, or delivers services. This latter can include distribution, eg the bloke who runs your local corner shop. A company, be it a private company or a public limited company, is merely a collection of individuals who do the same thing. In practice though, a company has shareholders, most of whom do not contribute to its wealth-creating processes, but simply own it and collect dividends. If the company goes bust, they will lose their investment, so it is in the interests of shareholders that it is managed efficiently.

Many capitalists are entrepreneurs, that is they start and run their own businesses. Some of them become famous, even achieving celebrity status. A few examples are Donald Trump – currently in the news; Oprah Winfrey – who went from hosting a talk show to media mogul; Richard Branson – who started out as a sole trader then built a massive business empire; and the inventor Clive Sinclair – whose son is likewise an inventor, his Babel bike was covered here in an earlier article.

Capitalists like the above create wealth, and by and large do not cause problems for the rest of us. Then there are the banks and the speculators. Broadly speaking, a bank has two legitimate functions: the bookkeeping function and the strongroom function, as discussed elsewhere. Banks also create credit. No, they do not lend money! As before, see elsewhere. According to standard economic theory, investment comes out of savings. While it is true that investment requires refraining from consumption to accumulate capital, in practice no investment is possible without somebody writing figures in a book, or today creating credit by pressing a few computer keys.

This was recognised as long ago as 1921 when this comment was directed at the Lloyd George Government: “Does he, and do his colleagues, realise that half a dozen men at the top of the five big banks could upset the whole fabric of Government finance by refraining from renewing Treasury bills?”

In fact, enlightened people have been aware of this from at least the early Nineteenth Century as the famous Guernsey Experiment proved. Most of the money created by the banks is done so not for productive purposes but for speculation, which is what caused the recent crashes, and along with speculators – to be discussed next – was responsible for the stock market crash of 1929.

Now we come to speculation. Most of the really big money is handled by managed funds: hedge funds, pension funds, unit trusts, and so on. What do these funds do? Ostensibly they pool the resources of the many to invest in the stock market, government bonds and such. But what do they really do? The bottom line is they gamble with other people’s money, day in, day out, year in, year out.

The prosaic reality of this was explained by Tony Levene in his classic book The Shares Game. These funds spend enormous sums of money on renting office space, paying economists, analysts, fund managers, advertising, etc, etc, but all they do is buy and sell. The people who run them produce absolutely nothing; any wealth they or their clients accumulate is at the expense of somebody else; that is not the way capitalism is supposed to work. You will find no Richard Branson among these people, certainly no Clive Sinclair, not even an Oprah. It is their ludicrous, incessant speculation that along with the banks causes almost all the problems capitalism and the economy face. Now that we have identified the causes of our malaise, what can we do to eradicate them?

The short answer is to take the power of credit creation away from the banks, and to eliminate speculation. As argued elsewhere, purchasing power belongs to producers, not to bookkeepers. The major single wealth-creator worldwide is the Internet, so internationally, the Internet rather than the commercial banks should have the power to create credit; in a nutshell, new money should be paid to the major ISPs and distributed to the major websites, who would further distribute to their major wealth-creators, from newspapers and publishers down to individual YouTube channels.

At a national level, the power to create credit would revert to the treasuries of the individual nations, something which may lead to the abolition of central banks. Credit used for government spending would be created responsibly debt-free by governments themselves, any excess credit issued being retired via taxation.

The elimination of speculation would be achieved by two measures: time constraints, and the break up of managed funds. Money zips around the globe in a nanosecond; when you make a card purchase in a store, the money comes out of your account and goes into the store’s account instantaneously. Likewise, trading on the world’s stock and commodities exchanges is instantaneous. Do you still have a cheque book? At one time, a cheque would take perhaps five days or more to clear. If all stock market transactions were made on the same basis, speculation would be drastically curtailed and prices would stabilise.

This delayed clearance could be augmented by a Tobin tax, something that was proposed way back in 1972 to combat currency speculation. Remittances from this would go to the treasuries of the respective nations.

As is made clear in Tony Levene’s aforementioned book, big funds are not simply useless but parasitic, so governments should close them all down and return their assets to the individuals who invested in them. These people would then have two options: to invest directly in the stock market themselves, or to pay their monies into a government holding fund that would not speculate, rather it would invest directly in the stock market – mostly blue chip companies – retaining a certain amount in cash to be paid out on demand. Finally, the governments of the world should take steps to reduce speculation in futures, and should eliminate derivatives completely.

One endnote, as banks would no longer be permitted to either create credit or pay interest on savings accounts, they would revert to their original functions as strongrooms and bookkeepers. Customers would therefore be required to pay for these services, probably on a transaction basic. This would effectively mean the end of free banking, but as is well known, there is no such thing as free in business – if you get something for nothing, somebody else is paying for it. Currently you pay for you rfree banking through taxation, something that will be greatly reduced and indeed will virtually disappear once we get the financial parasites off our backs.

To Wikinut Articles Page